Topwater Investments Monthly - May 2026

Quote of the Month

“Long-term success comes from balance and preparation, not reacting to short-term headline noise.” Larry Adam, Chief Investment Officer, Raymond James

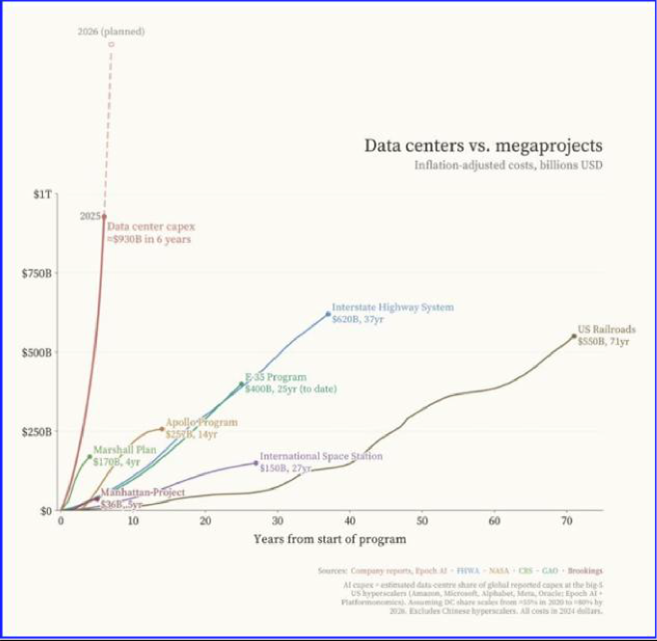

Chart of the Month

Message of the Month – April 2026 Letter from Raymond James Chief Investment Officer, Larry Adam.

Soccer legend Pele famously called soccer “the beautiful game”—a tribute to its universal accessibility, elegant simplicity, and strategic depth. All it takes is a ball, yet at its best, soccer becomes a shared global language, connecting players and fans across cultures and generations. That spirit will be on full display this summer as the US, Mexico, and Canada co-host the World Cup, with an estimated six billion viewers watching teams adapt to unfamiliar opponents, conditions, and tactics. The best players know talent alone doesn’t win tournaments—preparation, flexibility, and calm under pressure determine who advances.

The past year has demanded many of those same traits from investors. Rapid advances in artificial intelligence, persistent geopolitical tensions—particularly Iran—and ongoing trade uncertainty have kept headlines loud and emotions elevated. In that kind of environment, the biggest mistakes come from reacting to noise rather than fundamentals.

Like a well-organized team that keeps its composure over the full tournament—not just one match—investors who stay focused on long-term objectives and respond thoughtfully instead of emotionally are best positioned to succeed over time.

In the near term, developments in Iran will shape the economic outlook. Energy prices have reached multiyear highs, pressuring consumers. While the situation remains fluid, our base case is that the conflict will end shortly. Limited public support, rising gasoline prices, and shifting political momentum ahead of the midterm elections are likely to constrain its duration. Importantly, the impact on oil has been more about shipping disruptions than a significant loss of production. As conditions normalize, we expect oil prices to retreat toward $60 per barrel, reducing spillovers to economic growth, monetary policy, and asset markets.

Coming into the year, the US economy took the field in strong form. Still, as any soccer fan knows, matches can turn on a single moment—a deflection, a missed clearance, or a sudden counterattack. The recent spike in oil prices prompted a fresh review—our own Video Assistant Referee (VAR) moment—but the call stands: we still expect 2.4% economic growth in 2026.

Historically, oil shocks have been most damaging to weaker, energy dependent economies. Today, however, the US is on firmer footing: more energy efficient, less energy intensive, and a net exporter of oil, providing a stronger defensive line against supply disruptions.

Given our expectation of a brief conflict in Iran, higher oil prices appear to be a temporary headwind rather than a match-altering ‘red card.’

Consumer spending should remain supported by healthy tax refunds this season and improving hiring conditions, while business investment continues to benefit from record AI-related capital expenditures that are delivering the strongest productivity gains in two decades. While a prolonged rise in energy prices would raise recession risk, we see no reason to abandon our broader, more optimistic outlook based on a single contested play.

The Federal Reserve (Fed) is navigating this stretch with potential new leadership on the horizon, as Kevin Warsh sits a Senate confirmation vote away from becoming the next Fed chair. He appears well-suited for the coach’s role, bringing a rare blend of experience - firsthand knowledge of the locker room from his time as a Fed governor (2006–2011) and a clear understanding of how the crowd and markets react from his years on Wall Street.

That perspective matters. Still, once policy debates begin, the ultimate tempo of play is set by the full Federal Open Market Committee— the eleven other ‘players’ alongside the chair—and, as with any new leader, markets and fellow policymakers will quickly test his discipline, credibility, and consistency.

At present, the Fed faces a delicate tactical dilemma. Inflation remains stubbornly above the 2% target, constraining the Fed’s ability to ease, even as a softening labor market increasingly argues for eventual support. Geopolitical tensions and higher oil prices add near-term complexity and reinforce that restraint, but as those pressures fade later in the year, we expect the Fed to place greater weight on labor market conditions and deliver one rate cut before year-end.

In fixed income, bonds continue to play the role of the goalkeeper—steady and dependable when conditions get choppy. While inflation remains a risk, we do not expect elevated energy prices to persist, and with growth holding up, the 10-year Treasury yield should finish the year within our 4.25%–4.50% forecast range. Like a goalkeeper who favors control over power—calmly distributing the ball to reset play rather than forcing a booming kick—today’s starting yields are attractive, especially when compared to the historically low COVID-era levels. With monetary policy still mildly restrictive but gradually tilting toward easing, we continue to favor higher-quality bonds such as investment-grade bonds over riskier high-yield credit.

While the World Cup will capture global attention, many Americans dismiss soccer as “too boring.” But seasoned fans know the game isn’t just about goals; it’s about spacing, positioning, pace, and movement off the ball. Markets have looked similar this year: while the S&P 500’s pullback has been modest and its top-line trading range narrow by historical standards, a great deal of game-changing action has been unfolding beneath the surface.

Sector rotation has been meaningful. Energy surged early, while Financials lagged. We expect rotation to remain a defining feature of the equity market. Against geopolitical uncertainty and elevated energy prices, sectors with durable tailwinds and strong margins should prove most resilient. Technology remains the market’s captain, with Industrials,

Consumer Discretionary, and Health Care as our other star players. Technology benefits from sustained AI investment; Industrials from infrastructure, reshoring, and defense spending; Consumer Discretionary from moderating energy prices; and Health Care offers something akin to home-field advantage given its more domestic orientation and support from durable demographic trends. While Energy has been an early standout, we do not believe now is the time to increase exposure. As supply disruptions ease, recent outperformance may prove temporary—more like a breakaway run steadily closed down by disciplined defenders.

Volatility is likely to remain elevated in the near term, but investors should resist reacting to every whistle. The US economy remains on solid footing, and equities are entering this stretch from a position of strength. With valuations now more reasonable, we expect earnings growth of ~10% to carry the S&P 500 toward our year-end target of 7,250.

Importantly, that target is built on a conservative $300 earnings assumption—providing a meaningful cushion relative to the consensus forecast of $316.

Internationally, non-US equities were winners last year, aided by improving growth and a weaker dollar. Recently, however, a few ‘yellow cards’ have appeared. While the odds of winning the World Cup may favor teams like Spain, England, and France, we continue to prefer US equities over other developed international markets due to stronger GDP growth, more resilient earnings, and lower sensitivity to Middle East-related costs. In Asia, near-term volatility may persist, but we view these pressures as temporary setbacks. We remain constructive—though selective—on Asian emerging markets, where improving earnings momentum and solid longer term fundamentals, including exposure to the Technology sector, remain intact.

In soccer, the most reliable penalty kick isn’t the spectacular corner strike—it’s the calm kick straight down the middle as the goalkeeper commits one way or the other. Investing works much the same way. Long-term success comes from balance and preparation, not reacting to short-term headline noise. Over a full tournament—or a full market cycle—results are shaped by positioning and discipline. That’s where your advisor and our work help complete your team, maintaining perspective and increasing the likelihood of achieving your goals. In markets, as in soccer, championships are won by those who keep their composure, trust the process, and keep their eyes on the trophy. Wishing you an enjoyable World Cup. Go USA!

Lawrence V. Adam, III, CFA, CIMA®, CFP® Chief Investment Officer

Link to the full release of Raymond James’ Investment Strategy Quarterly: https://www.raymondjames.com/-/media/rj/common/investment-strategy-publications/investment-strategy-quarterly

As always, feel free to reach out if you have any questions regarding your investment strategy.

Thank you,

Colton Lightner, CFP®, AIF®

Financial Planner

Investment advice offered through Ascentis Independent Advisors (“Ascentis”), an investment adviser registered with the U.S. Securities and Exchange Commission. Topwater Capital, LLC is a DBA of Ascentis. Registration as an investment adviser does not imply a particular level of skill or training. The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.

Any opinions are those of the author and not necessarily those of Ascentis. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. All opinions are as of this date and are subject to change without notice. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not a guarantee of future results.

Investment Strategy Quarterly is intended to communicate current economic and capital market information along with the informed perspectives of our investment professionals. You may contact your financial advisor to discuss the content of this publication in the context of your own unique circumstances. Published 4/1/2026. Material prepared by Raymond James as a resource for its financial advisors.