Topwater Investments Monthly - April 2026

Quote of the Month

“A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at a good price.” Warren Buffet

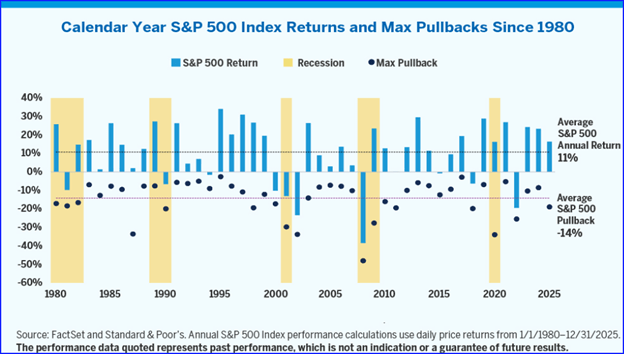

Chart of the Month

This chart shows that, since 1980, we have seen an annual S&P 500 pullback of 14% on average. During the same period, we have seen 11% positive annual returns on average. The message is, market pullbacks are part of investing, and we should view them as opportunities to increase our long-term investment returns.

Equity Indicators

Federal Reserve Policy.

The Federal Reserve held rates steady in their March FOMC meeting, with the fed funds rate remaining at 3.50 – 3.75%. Moving forward, the FOMC’s dot plot indicates one rate cut in late 2026 and one rate cut in 2027, after cutting rates three times in 2025.

Interest rate policy in 2026 will likely hinge on the length of the current conflict in the Middle East. The shock to oil prices brings the potential resurgence of inflation into focus. Some economists are more concerned that high oil prices could slow economic growth, if high gas prices eat into consumer spending, which makes up almost 70% of US GDP. This dynamic has brought about worries of “stagflation” – high inflation and low economic growth – like the US economy saw in the 1970’s. Fed Chair Jerome Powell indicated these concerns are overblown, given the current low unemployment rate and inflation around 3%, “What we have is some tension between the goals and we’re trying to manage our way through it” Powell added. “It’s a very difficult situation, but it’s nothing like they faced in the 1970’s and I reserve stagflation for that – the word – for that period. Maybe that’s just me.”

There is now a possibility that Jerome Powell has his term extended through January 2028. Nominee Kevin Warsh does not currently have a Senate confirmation hearing scheduled due to an ongoing DOJ probe into the Fed, which is being held up by appeals and a senator’s blockade.

Corporate Earnings.

As of 03/19/2026:

Earnings Growth: For Q1 2026, the estimated (year-over-year) earnings growth rate for the S&P 500 is 12.5%. If 12.5% is the actual growth rate for the quarter, it will mark the sixth-straight quarter of double-digit (year-over-year) earnings growth reported by the index.

Earnings Guidance: For Q1 2026, 50 S&P 500 companies have issued negative EPS guidance and 57 S&P 500 companies have issued positive EPS guidance.

Valuations.

As of 03/19/2026:

The forward 12-month P/E ratio for the S&P 500 is 20.3. This P/E ratio is above the 5-year average (20.0) and above the 10-year average (18.9).

Government Policy.

US and Israeli strikes on Iran in late February have created a complicated, global conflict in the Middle East. We believe this is one of those geopolitical events where it is best to wait and see how events progress, prior to making any major strategy adjustments. Given we saw this conflict as a strong possibility moving into 2026, we broadly initiated an overweight to the Energy sector in our strategies in late 2025 and plan to maintain the overweight for the time being.

Federal stimulus from the One Big Beautiful Bill Act (OBBBA) continues to be a consideration for our investment strategies, and we are primarily focused on the beneficiaries of increased infrastructure and defense spending.

On February 20, 2026, the U.S. Supreme Court ruled (6-3) in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose tariffs, striking down key components of President Trump's trade policies. The ruling maintains that Congress, not the executive branch, holds the power to tax and regulate commerce.

The administration has pivoted, replacing the struck-down tariffs with new, temporary tariffs under Section 122 of the Trade Act of 1974, which allows for temporary duties during balance-of-payments deficits. The administration continues to use other statutes, such as Section 232 (national security) and Section 301 (unfair trade), to continue a protective tariff policy.

Innovation.

Headlines pertaining to artificial intelligence (AI) have been focused on negative, extreme outcomes. A popular prediction is that we are all going to be replaced by AI agents and robots. Our view is more optimistic, as we hope for a gradual, positive implementation of AI into our society.

Using a historical reference, Johannes Gutenberg invented the movable type printing press around 1440. Seeing the potential mass market for printing in medieval Europe, numerous investors lent Gutenberg money for production. By enabling mass production of books, it enabled thinkers like Leonardo da Vinci and writers like William Shakespeare to influence a wider audience. The printing press acted as a primary catalyst for the Renaissance throughout the 15th and 16th centuries.

Like prior technological innovation, we believe AI will be an enhancement for humankind, not a replacement. One of our favorite metrics when analyzing a company is Revenue (Sales) per Employee. We have seen a significant increase in this metric among US corporations since AI adoption has accelerated. While corporations will likely need less employees, we believe human oversight, regulation, and ingenuity will always be necessary. And we believe many unforeseen opportunities will become available for our generation and future generations.

The long-term innovation trends we are focused on in our investment strategies include the AI infrastructure build-out, data management, cybersecurity, biotechnology/healthtech, automation/robotics, fintech, aerospace/defense, and energy.

Fixed Income Indicators

Yield Curve.

The current U.S. yield curve is slightly inverted, meaning short-term Treasury yields are higher than long-term yields, though it has recently shifted from a deeply inverted position to more of a Nike "swoosh" shaped curve. This shape reflects expectations for lower future interest rates over the next 2-5 years, while the long end of the curve, 10-year, 20-year, and 30-year yields remain elevated.

Credit Spreads.

High-yield spreads are the difference in yield between high-yield bonds and safer benchmark bonds, like U.S. Treasury securities and investment-grade bonds, and represent the extra return investors demand for taking on higher credit risk.

These spreads are currently more “tight” than historical averages, which indicates a higher level of investor confidence in higher-yielding bonds. We believe tight credit spreads reflect strong fundamentals, given corporate earnings growth and healthy corporate balance sheets.

As always, feel free to reach out if you have any questions regarding your investment strategy.

Thank you,

Colton Lightner, CFP®, AIF®

Financial Planner

Investment advice offered through Ascentis Independent Advisors (“Ascentis”), an investment adviser registered with the U.S. Securities and Exchange Commission. Topwater Capital, LLC is a DBA of Ascentis. Registration as an investment adviser does not imply a particular level of skill or training. The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.

Any opinions are those of the author and not necessarily those of Ascentis. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. All opinions are as of this date and are subject to change without notice. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not a guarantee of future results.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary.

https://davisfunds.com/education/wisdom-quotes

Diamond, J. (1997). Guns, germs, and steel: The fates of human societies. W.W. Norton & Company.